Skip to content

Skip to content A DWI arrest can be overwhelming, but you do not have to face it alone.

For many Texas drivers, the panic starts after they get home. You may be looking at bond paperwork, thinking about your license, and wondering whether Progressive will find out before you even have a chance to understand what happened. If you rely on your car for work, school, family, or court dates, that insurance question feels urgent.

That concern is not overreacting. A DWI case can affect far more than the criminal charge itself. It can affect your policy renewal, your premium, your SR-22 requirement, and in some cases your ability to keep financing or leasing a vehicle on stable terms. For CDL holders, the risk can be even more serious because a conviction can put your livelihood at risk.

Texas law moves quickly after an arrest. So do insurance consequences. The right response is not to guess, delay, or say too much too soon. The right response is to act strategically, protect your record where possible, and make every decision with both the court case and the insurance fallout in mind.

A DWI Arrest Is Overwhelming But You Can Take Control

The first night after an arrest usually feels like everything is happening at once. You may be thinking about the charge, your job, your family, and whether your insurance company is about to cancel you. If Progressive insures your car, one of the first questions is simple: what happens now?

Start with this. A Texas DWI is a criminal allegation that you operated a motor vehicle while intoxicated. A BAC, or blood alcohol concentration, is the alcohol level measured in your breath or blood. Implied consent means that by driving in Texas, you have already agreed to provide a breath or blood specimen if lawfully requested, though refusing can trigger separate license consequences. A field sobriety test is the set of roadside balance and attention tests officers use to build suspicion. An administrative license suspension is the separate civil process through the Texas Department of Public Safety that can affect your driving privileges apart from the criminal case.

Many drivers do not realize there are really two fights after a DWI arrest.

One is the criminal case. The other is the practical damage control that follows, including your driver’s license, your employment concerns, and your insurance position with a carrier like Progressive.

A smart response begins early:

- Protect your words: Do not call your insurer and start explaining the stop, the officer’s report, or what you drank.

- Protect your timeline: Texas license issues can move fast after an arrest, especially if there was a refusal or failed test.

- Protect your record: Insurance problems often become much worse after a conviction, not just after the arrest itself.

The strongest insurance strategy often starts in criminal defense. If the charge is reduced, dismissed, or weakened, the downstream damage may be very different.

People searching for a Houston DWI lawyer, a Texas DUI attorney, or guidance on how to fight DWI Texas are usually trying to solve a real-life problem, not just a legal one. They want to keep driving, keep working, and keep this from getting bigger. That is possible, but it takes a steady plan.

When and How Progressive Finds Out About Your DWI

Progressive usually does not learn about a Texas DWI because of one dramatic phone call. It is more often a chain of reporting events tied to your license status, court result, and policy activity.

The main ways notice happens

After an arrest, Progressive may learn about the matter through a few common paths.

A conviction hits your driving record

If the case ends in a qualifying conviction, that can appear on the record insurers review during underwriting or renewal.

An SR-22 becomes necessary

In Texas, some drivers must file an SR-22 to prove financial responsibility. Once that filing is required, your insurer becomes directly involved in that process.

You report it yourself

Some policyholders call too early and say too much. That can create unnecessary problems, especially when the criminal case is still developing.

A claim puts the event under a microscope

If the arrest involved a crash, vehicle damage, or injuries, the insurer may already be examining the incident from the claims side.

What to say and what not to say

You do not help yourself by speculating. If Progressive contacts you, keep your response short, accurate, and limited to what is necessary.

A practical script is often enough:

- Confirm identity and policy information

- Ask what specific information they need

- Avoid describing alcohol use or roadside statements

- Do not guess about charges, license status, or court outcome

- Say you are consulting counsel before giving a detailed statement

That matters because insurance questions are not always as simple as they sound. A “routine update” can turn into a statement that later conflicts with police reports, court filings, or a defense position.

If you have not spoken with counsel yet, do not try to explain the stop to your insurer from memory. Short, careful communication is usually safer than a long emotional account.

Why timing matters in Texas

A DWI arrest can trigger fast-moving deadlines. If your license is threatened, you may also be dealing with an ALR hearing, which stands for Administrative License Revocation. That hearing is separate from the criminal case and can be essential for fighting a DWI license suspension.

The sequence often looks like this:

- Arrest and release

- Temporary driving paperwork

- ALR deadline

- Criminal court settings

- Insurance review later, often at renewal or SR-22 stage

That is why a first DWI in Texas should never be treated as “just wait and see.” Delay helps the state, not you.

The hidden issue with financed or leased cars

Insurance consequences can also reach your vehicle loan. Progressive’s Loan/Lease Payoff coverage pays up to 25% of the vehicle’s ACV after a total loss, but it may not cover the full negative equity common in Texas and can involve exclusions for intentional illegal acts, as explained in this discussion of Progressive’s gap-style coverage. A DWI conviction can put that protection in question at the worst possible time.

If your case involved a wreck and you still owe heavily on the vehicle, that is not a minor detail. It is a financial risk that should shape your legal strategy from day one.

The Financial Fallout DWI Premium Hikes and SR-22 Filings

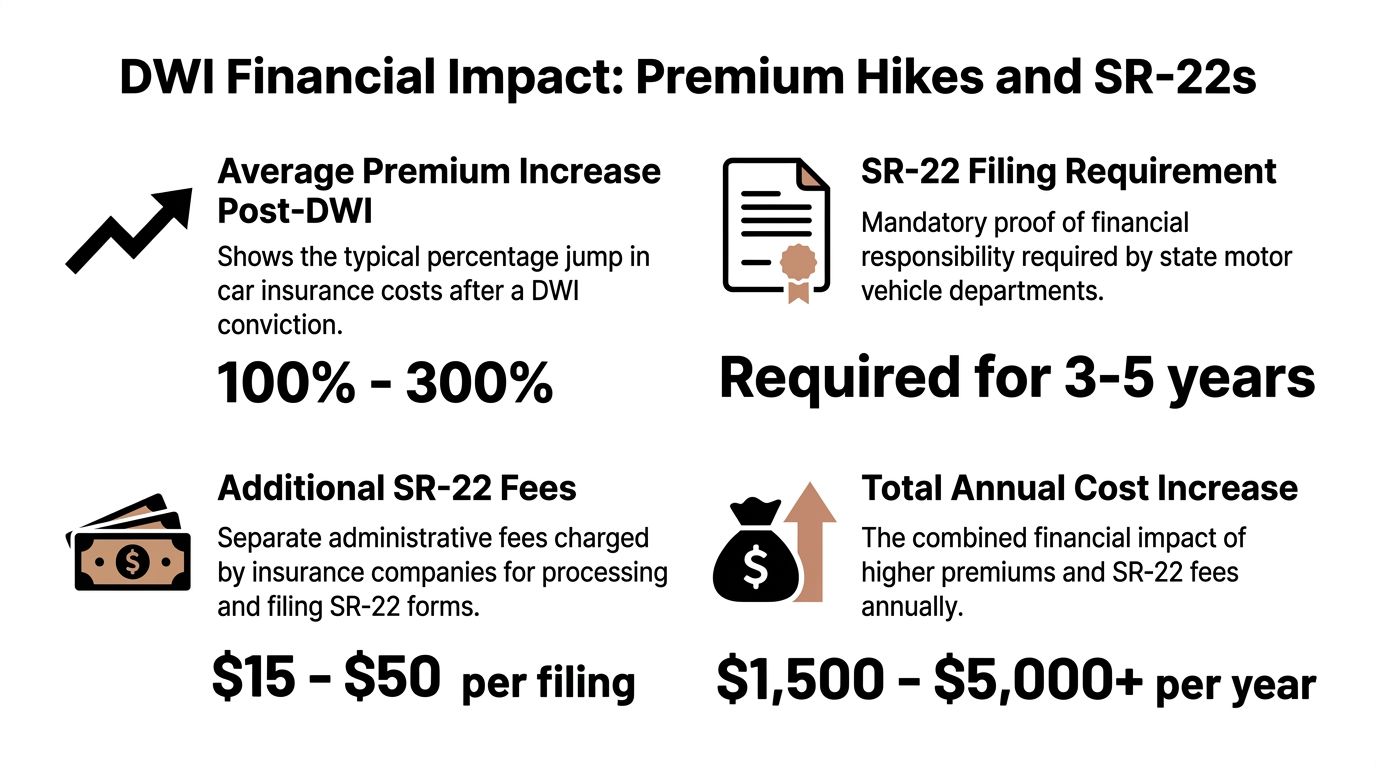

Most drivers ask the same question first: how bad will the insurance increase be?

The honest answer is that a conviction can be expensive, but Progressive is often less harsh than other major carriers for DUI-related pricing. That does not make a DWI harmless. It means smart planning can matter more than people think.

What a DWI surcharge really is

A surcharge is the additional premium an insurer applies because it now views the driver as a higher risk. With Progressive, the verified figures are more favorable than many competing carriers.

According to MoneyGeek’s analysis of Progressive car insurance cost, Progressive applies an average DUI surcharge of about $36 per month, bringing post-DUI full coverage to about $161 per month. The same analysis lists about $231 per month with GEICO and about $267 per month with Allstate after a DUI. The same source also notes a clean-record Progressive driver averages $125 per month, compared with a $136 industry average.

That difference matters if you need to keep a vehicle on the road while your case moves through court and DPS processes.

A quick comparison

| Insurer | Average Monthly Premium Clean Record | Average Monthly Premium After DWI | Estimated Monthly Surcharge |

|---|---|---|---|

| Progressive | $125 | $161 | $36 |

| GEICO | Not provided in verified data | $231 | Not provided in verified data |

| Allstate | Not provided in verified data | $267 | Not provided in verified data |

This is a useful starting point, not a guarantee for your exact case. Underwriting still depends on your history, location, vehicle, and policy details.

For a broader Texas-specific discussion of these pricing issues, this guide on DUI insurance surcharge in Texas explained is a helpful companion.

What an SR-22 is in plain English

An SR-22 is not a special insurance policy. It is a certificate your insurer files with the state to prove you carry the required financial responsibility.

In practice, it works like this:

- You are told that an SR-22 is required

- Your insurer files the form with the state

- You must keep the policy active

- If the policy lapses, the state can be notified

Progressive is known for handling SR-22 filings directly in Texas. That is one reason many high-risk drivers keep it on their short list after a DWI.

The video below gives a useful overview of how DWI consequences can affect your next steps.

Why fear gets people into trouble

The biggest financial mistake is not always the surcharge. It is the lapse.

Drivers sometimes panic, stop paying, or assume they will shop later. That can create a coverage gap at exactly the wrong time. If an SR-22 is involved, a lapse can trigger even more trouble with license reinstatement and make finding replacement coverage harder.

A better approach is to make decisions in this order:

- Keep the current policy stable unless you have a better option lined up

- Find out whether an SR-22 is required

- Coordinate insurance decisions with your criminal defense plan

- Do not assume the arrest and the conviction have the same insurance effect

The most expensive version of progressive insurance and dui is usually not the surcharge itself. It is a surcharge combined with a conviction, an SR-22 problem, and a policy lapse.

Will Progressive Drop You Understanding Cancellation and Non-Renewal

Many drivers assume one DWI means instant cancellation. That is usually too simplistic.

Cancellation and non-renewal are not the same

A cancellation happens during the active policy term. A non-renewal happens when the current term ends and the insurer chooses not to continue it.

That distinction matters. Mid-term cancellation is generally more restricted. Non-renewal gives the insurer more room to reassess the risk at the end of the term.

For Progressive policyholders, the better question is not “Will they drop me tonight?” It is “What will they do when they review this file?”

Why Progressive may keep the policy

Progressive’s underwriting approach is one reason many Texas drivers look there after a DUI. According to Scheuerman Law’s discussion of how long after a DUI insurance goes down, Progressive often applies an average 13% premium increase for a first-time DUI and tends to normalize rates within 3 to 5 years for drivers who keep a clean record. That pattern suggests a willingness to retain some drivers instead of immediately pushing them out.

That does not mean every driver stays insured without issue. It means the outcome is not automatic.

A first offense, stable payment history, and a clean post-incident record can matter. Repeated violations, serious aggravating facts, and policy problems can push the review the other way.

What helps and what hurts

A few practical factors often shape the insurer’s decision.

| Helps retention | Raises risk of non-renewal |

|---|---|

| First-offense posture | Repeated alcohol-related issues |

| Continuous coverage | Payment lapses |

| No new violations | New claims or violations after the arrest |

| Careful communication | Inconsistent statements |

If you want a closer look at that issue, this page on DUI insurance non-renewal Texas impact is worth reviewing.

A first-time DWI does not automatically mean Progressive will refuse to renew you. The result often turns on the full picture, not one label on one document.

Critical Issues for Texas CDL Holders and Leased Vehicles

Some drivers face much more than a higher premium. If you hold a CDL or drive a financed or leased vehicle, the insurance side of a DWI can become a career and asset protection problem.

CDL holders face a separate level of risk

Texas commercial drivers should not assume a personal auto policy solves the larger problem. It does not.

Progressive may issue an SR-22 for a personal vehicle, but that does not override commercial licensing rules. Under Progressive’s discussion of DUI and insurance issues, a first DWI conviction in Texas results in a mandatory one-year CDL disqualification under Transportation Code §521.204. For many drivers, that situation represents the primary emergency.

If you drive for a living, the case is not just about a fine or your personal car insurance. It is about whether you can continue working in the field at all.

That is why CDL defense needs to be immediate and aggressive. A plea that may look manageable for another driver can be devastating for someone whose income depends on a commercial license.

For more on that overlap, see this page on DUI commercial insurance Texas impact.

Leased and financed vehicles create another layer

Now add a lender or leasing company.

A DWI-related crash can trigger questions about total-loss handling, payoff limits, and whether optional protection fills the gap you thought it would. With financed vehicles, the driver often worries about one thing: “If the car is totaled, will insurance pay off what I still owe?”

The answer can be less comforting than expected.

Here are the practical pressure points:

- Loan balance risk: If the car’s value drops below the loan balance, you may still owe money after a total loss.

- Coverage exclusions: DWI-related facts can lead to disputes over what is covered in a particular situation.

- Lease obligations: Leasing contracts may create obligations that continue even while the criminal case is pending.

Why these cases need a different strategy

A generic “let’s just work something out” approach can be costly for these drivers.

For CDL holders, the target is often to avoid the conviction itself if the facts and law support that fight. For financed or leased vehicles, the goal is to keep the case from snowballing into a license problem, an insurance problem, and a vehicle debt problem at the same time.

If your situation falls into either category, move quickly on three fronts:

- Get the arrest paperwork organized

- Confirm your current insurance status

- Review any lease or financing documents for loss and coverage terms

Those documents can shape what matters most in negotiations and defense planning.

Your Proactive Defense Limiting Insurance Damage and Protecting Your Future

The best way to manage progressive insurance and dui consequences is to attack the legal case early. Insurance damage is often downstream from legal damage. If you improve the court outcome, you may improve the insurance outcome too.

Start with the two-track process

After a Texas DWI arrest, you are dealing with two separate systems.

The first is the criminal case. That is where the state tries to prove intoxication.

The second is the administrative license process. If your breath test was refused or failed, the state may try to suspend your license through the ALR process. That is why requesting an ALR hearing quickly matters. It can preserve your ability to drive and create an early opportunity to examine the officer’s basis for the stop and arrest.

If you are trying to understand the sequence, it often includes:

- Arrest and booking

- Bond conditions

- Temporary driving privilege paperwork

- ALR hearing deadline

- Court appearances

- Negotiation, motions, or trial preparation

Each stage can affect the pressure on your insurance position.

Know the defense issues that can change outcomes

Not every arrest leads to the same result. A strong Texas DUI attorney looks closely at how the stop happened and what evidence the state really has.

Possible issues include:

- Reason for the traffic stop: Did the officer have lawful grounds to pull you over?

- Field sobriety testing: Were the tests administered correctly, and do the bodycam and report match?

- Breath or blood evidence: Was the sample obtained lawfully, and was the machine or process challenged?

- Officer observations: Are the claimed signs of intoxication specific and credible, or broad and inconsistent?

Those are not technicalities. They are the foundation of the state’s case. Weakness there can provide an advantage in negotiations or support a stronger motion strategy.

What you should gather right away

Do not wait for memory to fade.

Collect and save:

- Bond paperwork

- Notice related to license suspension

- Tow or impound papers

- Insurance declaration page

- Lease or financing agreement if applicable

- Names of any passengers or witnesses

- Your own written timeline of the stop, arrest, and release

Keep that file organized. It helps both your defense and your insurance planning.

Write your timeline while the details are fresh. Include where you were, what you ate, what you drank if anything, what the officer said, and whether any testing was requested or refused.

Why charge reduction and dismissal matter so much

Drivers often focus only on the short-term court date. The bigger picture is the record that follows you.

A reduced charge, a dismissal, or a case problem that weakens the state’s proof may change whether the harshest insurance consequences are triggered. That is one reason the phrase fight DWI Texas should mean more than showing up and hoping for the best. It should mean building a stronger position from the first week of the case.

For some drivers, an outcome short of a DWI conviction can make a meaningful difference in future underwriting, licensing, and employment concerns. The exact impact depends on the final record and the insurer’s review, but the legal result matters.

Use clean driving to rebuild after the case

If the case has already reached the point where insurance consequences are in play, there is still a path forward.

Progressive’s auto discounts and Accident Forgiveness options can help drivers who stay violation-free after the incident. The company offers forms of Accident Forgiveness, including Small Accident Forgiveness, and those benefits can keep a later minor claim from causing another rate increase.

That is important because recovery is usually not one dramatic event. It is a series of disciplined choices:

- Keep coverage active

- Avoid new tickets

- Do not let the SR-22 process lapse if one is required

- Follow every court order

- Drive like your record matters, because it does

Understand key terms before you make decisions

A few definitions can keep you from making costly assumptions.

Implied consent means Texas drivers can face consequences for refusing a lawful breath or blood request.

BAC is the measured alcohol concentration in your breath or blood, but a DWI case can still involve legal disputes about how that evidence was obtained and interpreted.

Field sobriety tests are roadside exercises officers use as investigation tools. They are not the same thing as a laboratory result.

Administrative license suspension refers to the DPS process that can affect your license outside the criminal courtroom.

Understanding those terms makes it easier to make smart decisions about whether to request hearings, challenge evidence, or avoid statements that lock you into a weak position.

Think beyond the criminal charge

Many people start this process by worrying about jail, then later realize the most significant damage may be financial and professional. Insurance costs, renewal problems, CDL consequences, and vehicle loan exposure can last much longer than the night of the arrest.

That is why the right defense is both legal and practical. It aims to protect your license, reduce record damage where possible, and prevent the case from triggering avoidable insurance fallout.

If you are facing a first DWI in Texas, do not assume the least resistance is the safest path. In many cases, the cheapest-looking short-term decision becomes the most expensive long-term one.

Take Control of Your Case with a Houston DWI Lawyer

A DWI charge can feel like it put your whole future on hold. That feeling is common, especially when you are worried about your license, your job, and what Progressive may do with your policy. But this is the point where clear legal strategy matters most.

Texas DWI cases are not only about what happened on the roadside. They involve the stop, the testing, the officer’s report, the ALR process, the criminal court process, and the practical fallout that can affect your insurance and daily life. If you try to handle all of that alone, it is easy to miss a deadline or make a statement that hurts you later.

A Houston DWI lawyer can evaluate whether the stop was lawful, whether the testing can be challenged, whether your DWI license suspension can be contested, and what outcome gives you the best chance to protect your record. That matters whether you are dealing with a first offense, a CDL problem, or a leased vehicle that adds financial pressure.

If you are searching for a Texas DUI attorney, the right next step is simple. Get legal advice before you talk too much, plead too fast, or assume the insurance damage is already locked in. In many cases, it is not.

You can fight this case. You can protect your position. And you can make informed decisions that help preserve your license, your finances, and your future.

If you are facing a DWI in Texas and need clear answers now, contact Law Office of Bryan Fagan, PLLC for a free, confidential consultation. Our team helps drivers across Texas challenge DWI allegations, fight ALR hearings, protect against license suspension, and pursue outcomes that reduce the long-term damage to your record, your insurance, and your career.