A DWI arrest can be overwhelming—but you don’t have to face it alone. Beyond the immediate stress of the legal system, you’re likely worried about the long-term consequences, especially for your finances. A common question we hear is: how long does a DWI really affect your insurance?

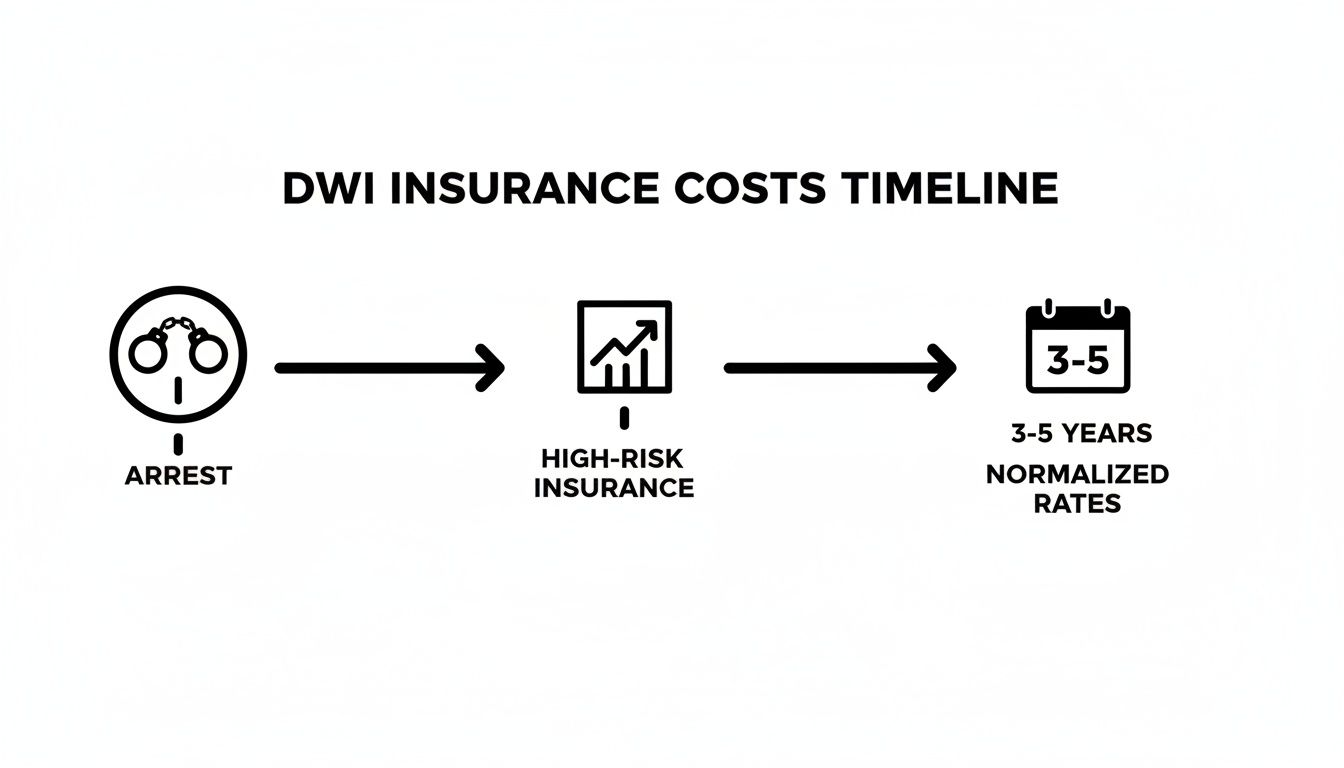

In Texas, you can expect a DWI conviction to impact your insurance rates for at least three to five years, and sometimes even longer. This isn't just a temporary inconvenience; it's a long-term financial reality that redefines you as a "high-risk" driver in the eyes of every insurance company. However, with a strategic legal defense, it’s a reality you may be able to avoid.

The True Cost of a DWI on Your Texas Insurance

Facing a DWI arrest is a confusing and isolating experience. While the legal process feels like the most immediate battle, the financial consequences often have the longest reach. A conviction doesn't just mean fines and potential jail time—it kicks off a domino effect that will impact your auto insurance for years to come.

The moment an insurer sees a DWI conviction on your driving record, they no longer see you; they see a statistic. You are immediately reclassified from a standard driver to a high-risk driver. This isn't a personal judgment. It's a business decision based on data linking DWI convictions to a much higher likelihood of future accidents and expensive claims. This new label is precisely why your premiums can skyrocket.

The Financial Fallout of a High-Risk Label

Being labeled "high-risk" isn't a one-time penalty. It's a sustained financial burden that can stick with you for years, long after your legal case is resolved.

Here’s a clear look at what to expect:

- Massive Premium Hikes: It's common for drivers to see their annual premiums double or even triple. An increase of 70% or more is standard in Texas after a first DWI.

- Loss of All Your Discounts: Say goodbye to the "good driver," "safe driver," and "claims-free" discounts you earned. They will likely be wiped out, pushing your new, higher rates even further up.

- Getting Dropped by Your Insurer: Your current insurance company might decide you're too risky to cover. They can refuse to renew your policy, forcing you to find new, and almost certainly more expensive, coverage.

- The SR-22 Requirement: The state will mandate that you file an SR-22 certificate. This document proves you carry liability insurance and serves as a bright red flag to the insurance industry that you are a high-risk driver.

The timeline below breaks down what this financial journey typically looks like after a DWI conviction in Texas.

Texas DWI Insurance Impact Timeline

| Timeline Phase | Typical Duration | Key Insurance Impact |

|---|---|---|

| Immediate Aftermath | 0-3 Months | Policy non-renewal is common. You will be required to file an SR-22, and your search for new insurance begins in the high-risk market. |

| The Peak Impact | Years 1-3 | This is when you'll feel the most financial strain. Premiums can be 2-3 times higher than before the DWI. All safe-driver discounts are gone. |

| Gradual Improvement | Years 3-5 | If you maintain a clean record, some insurers may begin to lower your rates slightly, but you are still considered high-risk. |

| Returning to Normal | Year 5+ | After five years with no new incidents, you may finally be able to qualify for standard rates again and shed the high-risk label. |

This table shows a clear, multi-year financial struggle. It's not just a single bill; it's a long-term consequence that costs thousands.

A DWI conviction is more than a mark on your record; it's a multi-year financial event. Avoiding that conviction is the single most effective way to protect yourself from thousands of dollars in increased insurance costs.

The road ahead might seem daunting, but a strategic legal defense can make all the difference. As you can explore further in our guide to insurance premiums after a DUI in Texas, taking proactive steps with an experienced attorney is crucial. By fighting the charge itself, you fight to prevent the conviction that triggers these long-term financial penalties in the first place, safeguarding not just your driver's license but your financial future.

Why Your Insurance Premiums Will Increase After a DWI

When your insurance bill suddenly doubles after a DWI, it’s easy to feel like you’re being personally punished. The truth is, it’s not personal at all—it’s business. Insurance companies run on data, using actuarial tables to predict the likelihood of a future claim. A DWI conviction completely rewrites your risk profile.

From an insurer's point of view, a DWI on your driving record instantly moves you from the "standard driver" category to the "high-risk driver" pile. This isn't about judgment; it's a direct response to statistics. Data shows that drivers with a history of driving while intoxicated are more likely to be involved in future accidents, which means expensive payouts for the insurance company.

This timeline breaks down how a single DWI conviction can trigger that high-risk classification and keep your insurance costs inflated for years to come.

As you can see, the financial pain isn't a quick sting. It’s a sustained issue that typically lasts for a minimum of three to five years before your rates even begin to return to normal. Understanding the "why" behind this rate shock is the first step toward realizing how much a strong legal defense makes financial sense.

The Math Behind the Rate Hike

Insurance companies translate this new, higher risk directly into dollars and cents. The exact premium increase will vary depending on your provider, your past driving record, and other personal factors, but you can count on it being substantial. They are simply adjusting your price to cover the higher potential cost you now represent to them.

Think of it this way: before the DWI, your insurer saw you as a safe bet. Now, they see you as a gamble, and they’re increasing the cost to protect their bottom line. This is why even a first-time DWI in Texas can leave such a deep and lasting crater in your budget.

Real-World Examples of DWI Insurance Increases

The numbers are often jarring. Seeing the actual data from major insurance providers paints a much clearer picture of the financial storm a DWI conviction can unleash. And make no mistake, some companies are far more aggressive with their rate hikes than others.

Recent data analysis, for example, shows some staggering jumps. A driver with Amica Mutual could watch their average annual rate of $1,318 explode to $3,511—a 166% increase. A Nationwide customer might see their rate leap 125%, from $1,475 to $3,315. On average, drivers can expect to pay about $1,657 more per year for full coverage, which is a 72% increase.

When you remember this financial penalty sticks around for several years, a single DWI could easily cost you between $8,000 and $16,500 in extra insurance premiums alone. You can exploring the full data on DUI insurance rates to see more details on how these increases play out.

Why a Conviction Is the Trigger

Here’s the most critical piece of the puzzle: insurance companies react to convictions, not arrests or charges. An arrest is just an accusation. A conviction, on the other hand, is a legal judgment that gets stamped onto your official driving record—a record that insurers check regularly, especially when it’s time to renew your policy.

This distinction is the absolute cornerstone of an effective defense strategy. If you can prevent a conviction—whether through a case dismissal, a reduction to a non-alcohol-related offense, or an acquittal at trial—you can stop this entire insurance nightmare before it even starts.

This is precisely why getting an experienced Houston DWI lawyer involved immediately after an arrest is so vital. The entire goal is to dismantle the state's case and fight to avoid the one thing that triggers all these long-term financial consequences: the conviction. Protecting your driving record is the best way to protect your wallet.

Navigating the Texas SR-22 Requirement

After a DWI conviction, a new term will likely enter your vocabulary: the SR-22. It’s a requirement that can cause anxiety, but once you understand what it is—and what it isn't—you can manage the situation with confidence.

Let's clear up the biggest misconception. An SR-22 is not an insurance policy. It's simply a certificate, a form that your insurance company files for you with the Texas Department of Public Safety (DPS). Think of it as a special alert on your driving record that tells the state, "This person is insured, and we are monitoring their coverage."

Who Needs an SR-22 and for How Long

In Texas, an SR-22 is standard procedure after a conviction for a serious traffic offense like a DWI. The court or the DPS will notify you if it's required. The rule is simple, but it’s incredibly strict.

You are required to maintain continuous SR-22 coverage for two years starting from the date of your DWI conviction. This two-year clock is absolute and watched closely by the DPS.

And "continuous" is the key word. If your policy lapses, even for a single day, your insurance provider is required by law to notify the DPS immediately. That notification triggers an automatic re-suspension of your driver's license, creating a new legal issue to resolve.

How to Get an SR-22 in Texas

While the SR-22 sounds intimidating, the process of getting one is fairly straightforward, though it does have a financial cost. Here’s what you’ll need to do:

- Contact Your Insurance Company: You’ll need to inform your current agent that you have an SR-22 requirement. Be prepared—not all companies will file them, and you may need to shop for a new insurer that specializes in high-risk drivers.

- Pay the Filing Fee: Your insurer will charge you a small, one-time fee to file the certificate with the DPS. This usually runs between $15 and $50.

- Prepare for Higher Premiums: This is the part that hurts. Needing an SR-22 officially places you in the "high-risk" category, and it’s the trigger for the major premium hikes discussed earlier.

- Keep Your Proof: Once the form is filed, your insurer will give you a copy. Keep it in your vehicle at all times as proof that you are complying with state law.

The SR-22 is a critical but manageable piece of the puzzle after a DWI. Staying on top of your obligations is the only way to protect your driving privileges. For a deeper look at this, our detailed guide explains more about how an SR-22 can affect a suspended license in Texas.

Of course, the best way to deal with the SR-22 headache is to avoid it in the first place. A conviction is what sets this all in motion, which means fighting the DWI charge itself is the most effective way to avoid the fees, filings, and financial fallout.

Hidden Costs and Long-Term Consequences of a DWI

The sticker shock from a higher insurance premium is bad enough, but it’s often just the beginning. Think of a DWI conviction like a stone tossed into a pond. The initial splash is that first rate hike, but the financial ripples spread out much wider—and last far longer—than most people expect. Understanding these hidden costs is key to grasping why fighting the charge from day one is so critical.

One of the most immediate impacts can be a non-renewal notice from your insurance company. After a DWI conviction, many standard carriers may decide you're too big of a risk. They can drop your coverage, forcing you into the high-risk insurance market, where options are limited and prices are much higher.

The Slow Bleed of Lost Discounts

Beyond the base rate increase, a DWI conviction also systematically wipes out the valuable discounts you’ve earned over the years. You might not notice them until they're gone, but their loss quietly adds up, inflating your costs month after month.

You can likely say goodbye to:

- Good Driver Discounts: This is the first to go. A DWI immediately disqualifies you.

- Claims-Free Rewards: Your history of being claims-free is overshadowed by the new high-risk label.

- Good Student Discounts: If you or another driver on your policy had this, it is almost certainly gone.

- Multi-Policy Bundles: Some insurers won’t bundle home or renter’s insurance with a high-risk auto policy, meaning those savings evaporate.

This isn’t just about paying a higher premium. It’s about your entire insurance profile being re-evaluated and stripped of its value. The financial damage compounds for years, and you can learn more by reading our guide on the hidden costs of a DUI charge.

The Ripple Effect on Your Financial Life

The ripple effect from a DWI can destabilize your financial life. Many insurers will cancel your policy or refuse renewal, leaving you scrambling. This forces you into a high-risk market where costs are punishing and choices are few. This is made worse by the loss of every discount that once made your policy affordable. The sobering statistics from the National Highway Traffic Safety Administration—which report nearly 10,000 deaths in alcohol-related crashes each year—show exactly why insurers take DWI convictions so seriously. You can discover more about how these ripple effects impact insurance rates to understand the full scope of the fallout.

A DWI conviction doesn't just raise your rates—it can make you uninsurable with standard carriers and erase years of good-driver status overnight.

Fighting the charge isn't just about avoiding fines or jail. It’s about containing this financial bleeding. An experienced Houston DWI lawyer works to prevent the conviction that sets these devastating ripples in motion in the first place. By challenging the state’s case, we aim to protect not just your driving record, but your entire financial well-being from the long-term damage of a single mistake.

How a Strategic Defense Protects Your Driving Record and Rates

So far, we’ve focused on the problems a DWI conviction causes for your insurance. Now, let's shift to the most important part of this discussion: the solution. A DWI charge does not have to end in a conviction, and that fact is the key to protecting your driving record and keeping your insurance rates from spiraling out of control.

Insurance companies only care about one thing: a conviction. An arrest is just an accusation; a conviction is a final legal judgment that gets stamped on your permanent driving record. A strategic defense, led by an experienced Houston DWI lawyer, is designed to stop that conviction from ever happening. It cuts the problem off at the source. If there's no conviction, your insurer has no grounds to raise your rates or drop your policy.

How Your Attorney Fights the Charge

A skilled Texas DUI attorney doesn’t just accept the state’s version of events. Instead, we meticulously dismantle every piece of the prosecution's case, searching for weaknesses, procedural mistakes, and violations of your rights. This is how we build a path toward a positive outcome and protect your financial future.

Here are some ways we challenge the core elements of a DWI arrest:

- The Initial Traffic Stop: Did the officer have a legal reason—known as "reasonable suspicion"—to pull you over in the first place? If not, any evidence gathered afterward could be thrown out of court.

- The Field Sobriety Tests: These tests are notoriously subjective and often administered improperly. We scrutinize the officer’s actions, looking for any deviation from standardized procedures that could make the results unreliable.

- The Breath or Blood Test: We dig into the details. For blood tests, we examine the chain of custody. For breathalyzers, we check the machine’s maintenance and calibration records. Any errors can render the test results inadmissible.

By aggressively questioning the evidence, we create the leverage needed to negotiate with the prosecutor or build a powerful case for trial.

The goal of a strong DWI defense is not just to "get you off"—it is to protect your entire future. Preventing a conviction saves you from years of inflated insurance premiums, license suspensions, and a permanent mark on your record.

The Power of a Dismissal or Reduction

The absolute best outcome is getting the charges dismissed completely. When that happens, it’s as if the arrest never occurred from an insurance company's perspective. No conviction, no SR-22, and no reason for your rates to climb.

Another highly effective strategy is negotiating to get the charge reduced to a non-alcohol-related offense, like reckless driving or obstruction of a highway. While a reckless driving ticket isn’t a win for your insurance, its impact is far less severe and doesn't last nearly as long as a DWI. It allows you to sidestep the automatic "high-risk" label and the mandatory SR-22 filing that a DWI conviction triggers.

Winning the ALR Hearing Is the First Step

Your defense starts long before you ever step into a criminal courtroom. You have just 15 days from the date of your arrest to request an Administrative License Revocation (ALR) hearing. This is your chance to fight the automatic DWI license suspension.

Winning this hearing can be the first domino to fall in a successful defense strategy. It gives us an opportunity to cross-examine the arresting officer under oath, locking in their testimony and often exposing critical weaknesses in the state’s case. A victory at the ALR hearing not only saves your license but also gives us powerful momentum as we move into the criminal proceedings.

Investing in a robust legal defense is a direct investment in your financial stability. By working to avoid a conviction, you are actively preventing the thousands of dollars in premium hikes that would otherwise follow you for years. A skilled Houston DWI lawyer can help you fight DWI Texas charges and safeguard your future.

Taking Proactive Steps to Safeguard Your Future

After a DWI arrest in Texas, it’s natural to feel like everything is spinning out of your control. But you have more power in this situation than you might think. While the potential consequences for your insurance are serious, the final outcome isn't set in stone. The most critical decision you can make right now is to act quickly and strategically.

Taking proactive steps is the only way to protect your future from the long-term financial fallout of a DWI conviction. This means understanding your rights, knowing the process, and—most importantly—partnering with a skilled legal advocate who can fight for you. You don't have to walk through this confusing legal and financial maze alone.

Your Next Steps are Crucial

The moves you make in the hours and days after an arrest can dramatically change the trajectory of your case. Don't wait for the state to build its case against you. By taking immediate action, you put yourself in the strongest possible position to defend your rights and your financial future.

Here’s your immediate game plan:

- Preserve All Evidence: Write down every detail you can recall about the traffic stop, the field sobriety tests, and your arrest. Memories fade quickly, but these details can become invaluable evidence later.

- Request Your ALR Hearing: Remember, you only have 15 days to request an Administrative License Revocation (ALR) hearing. This is your one chance to save your license from automatic suspension, and that deadline is non-negotiable.

- Consult a DWI Attorney: This is the most important step you can take. A skilled Texas DWI lawyer can get involved immediately, ensuring all deadlines are met and your rights are protected from the very beginning.

Understanding the Financial Stakes

The financial impact of a DWI conviction is both immediate and significant, and it goes far beyond court fines. Recent data shows that Texas drivers with a full-coverage policy can expect an approximate 62% rate increase after a conviction. This isn't just an annoyance; it's a multi-year financial burden that can cost you thousands.

When you add in attorney fees, court costs, and fines, the total out-of-pocket expense for a single DWI can easily fall between $10,000 to $25,000. To get a better handle on how a DWI conviction impacts insurance rates and personal finances, you can find more about these financial consequences and timelines.

A DWI charge feels overwhelming, but remember this: an arrest is not a conviction. You have the right to fight, and a strong defense is your best shield against lasting financial penalties.

At The Law Office of Bryan Fagan, PLLC, we understand the anxiety and uncertainty you're facing. Our team of experienced Houston DWI attorneys is here to provide the strategic, reassuring guidance you need. We will meticulously review every detail of your case, protect your rights at every turn, and build a defense aimed at securing the best possible outcome.

Don't let a DWI charge define your future. Contact us today for a free, confidential consultation to discuss your case and learn how we can help you move forward.

Frequently Asked Questions About DWI and Insurance

A DWI charge can throw your life into chaos, and the questions may feel overwhelming. Beyond the legal battle, you're probably worried about practical, everyday things—like your car insurance. How bad is it going to get?

Here are some of the most common questions our clients ask about DWI and insurance, with the clear, professional answers you need to see the path forward.

If My DWI Is Dismissed, Will My Insurance Still Go Up?

This is a critical question, and the answer is usually a huge relief: No. Insurance companies increase your rates based on convictions, not arrests.

When your Houston DWI lawyer gets your case dismissed or you are found not guilty at trial, there is no conviction for the insurance company to act on. From their perspective, it's as if it never happened. This is the best-case scenario. It keeps your driving record clean, avoids the SR-22 requirement, and gives your insurer no legal reason to touch your premiums. This is precisely why fighting the charge from day one is so crucial for your financial health.

Can I Switch Insurance Companies to Get a Lower Rate After a DWI?

You can always shop around, but don't expect a magic solution. Once you have a DWI conviction, it becomes part of your official driving record. Every insurance company will see it the moment you ask for a quote.

That conviction will follow you, no matter where you go. While some companies specialize in high-risk drivers and might offer a slightly better deal than your current provider, you are still going to be paying significantly more than you were before. It’s always smart to compare quotes, but the only truly effective way to keep your rates from skyrocketing is to avoid the conviction entirely.

The Bottom Line: There's only one guaranteed way to stop a DWI from impacting your insurance rates—prevent the conviction. A dismissal or acquittal means your insurer has no grounds to penalize you.

How Long Do I Need an SR-22 in Texas?

In Texas, if you are convicted of a DWI, you will be required to maintain an SR-22 for two years from the date of your conviction. The SR-22 is a certificate of financial responsibility that your insurance company files on your behalf.

It is absolutely critical that you do not let your policy lapse during this two-year period—not even for a day. If your coverage is canceled or expires, your insurance company is required by law to immediately report it to the Texas Department of Public Safety (DPS). That report automatically triggers a new suspension of your driver's license, and you will be facing another legal headache.

Does a Defensive Driving Course Lower My Insurance After a DWI?

Taking a defensive driving course is a positive step, and a judge might even order you to complete one. However, when it comes to your insurance premiums after a DWI conviction, its impact is minimal at best.

Some insurers might offer a small discount for finishing an approved course, but it will not be enough to offset the massive surcharge you’ll receive for the DWI. A conviction places you in a high-risk category that a weekend driving class simply can't erase. The premium hike is a business decision based on risk, and that's not something you can reverse with a certificate of completion.

A DWI arrest can make you feel like the weight of the world is on your shoulders, but you don’t have to carry it by yourself. At The Law Office of Bryan Fagan, PLLC, our experienced Texas DWI attorneys are here to provide the strategic, confident defense you deserve. We will fight to protect your rights, your license, and your financial future. Contact us today for a free, confidential case evaluation and find out how we can start fighting your charges. https://texasduilawfirm.com